Unlike market peaks, when positive sentiment easily supports staying in the game, a market drawdown leads many to question portfolio exposure to equity. Fears of further downside to come not only leave many hesitant to retain an existing strategy; they can push some to throw in the towel altogether. In squishier times like these, when the pressures driving market declines are more difficult to pin down, it can be particularly challenging to find reasons to keep a steady hand, let alone be optimistic. We think the simplest, most powerful reasons are:

- Having proved unable to time the peak, one is unlikely to be able to time the bottom

- History suggests that decisions to unwind stock exposures in the wake of market downturns tends to prove detrimental to financial outcomes

- Missing out on potential upside ultimately may prove more painful

Listen to this month's Notes from the CIO podcast:

Podcast: Play in new window

We Saw It Coming...

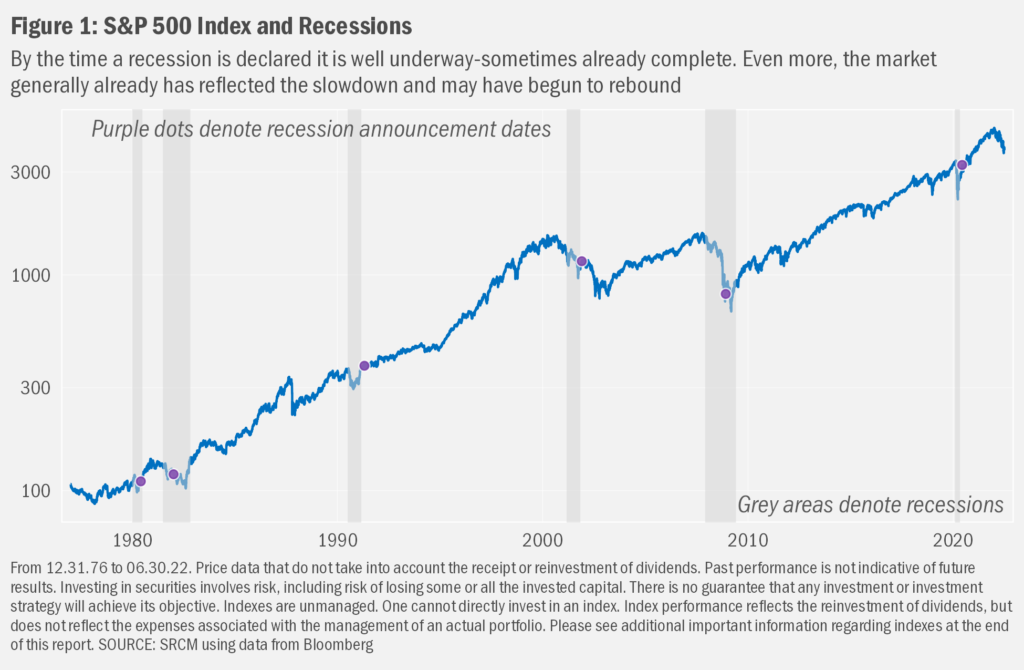

According to the entity charged with delineating economic cycles, the National Bureau of Economic Research (NBER), “a recession is a significant decline in economic activity spread across the economy, normally visible in production, employment, and other indicators. A recession begins when the economy reaches a peak of economic activity and ends when the economy reaches its trough.” Over the past half-century, a market drawdown has preceded the declaration of every recession. But this makes sense. Markets generally get ahead of an eventual recession determination as investors digest whiffs of uneasiness that turn into anecdotes of slowing trends that in time become data that reflect a slowing of the broader economy across many metrics. Given that lag, we only learn of the fact of a recession well after one’s already begun. Sitting more than 20% below the market peak set back in January, then, as we ask ourselves whether the U.S. has or will enter into a recession, we should accept that the market seems to suggest that the answer is yes.

..Now What?

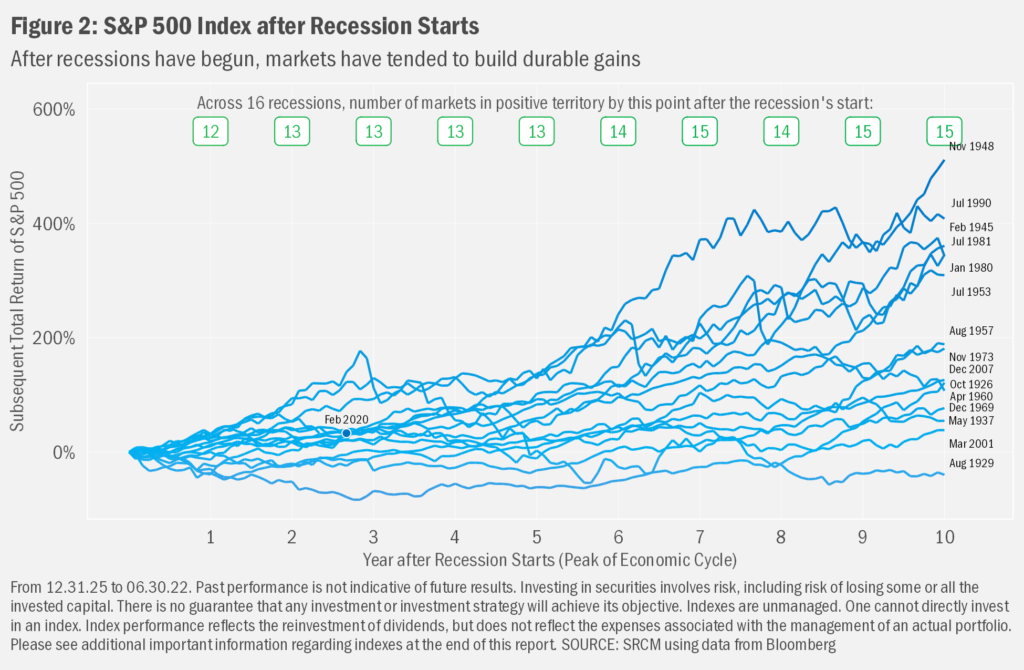

Like we said, a stock market downturn generally precedes the actual announcement of a recession, as investors react to changes in data trends that form the basis for the eventual declaration that a recession has occurred. As is now the case, when it seems the market already reflects a sense that a recession is in the offing, we have found it a particularly opportune time to revisit a basic premise of investing: that all investing carries risk, but that investors tend to be rewarded for patience during times of market stress. Historical patience even against a potential current or oncoming recession supports that tenet. Across 16 recessions over the past near century of data that we show in Figure 2, once a recession has begun, the market’s been rather quick to provide durable gains. Acknowledging that in most cases the market is off a prior peak once the recession has started (look back to Figure 1), investor patience may allow those gains to offset those earlier losses, then potentially rally into positive territory over time.

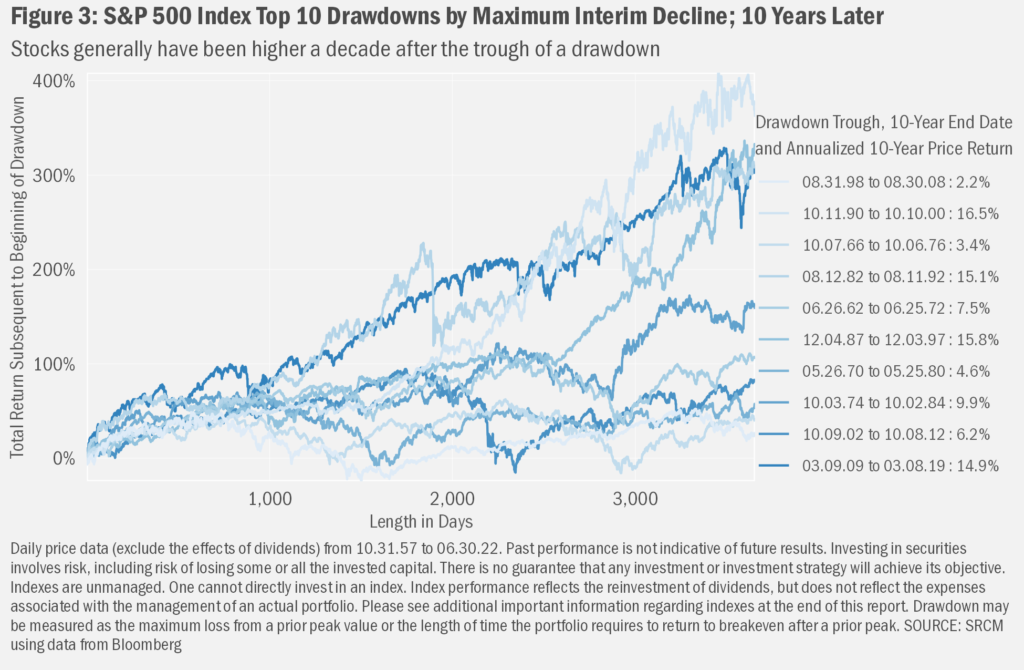

This tends to have been true whether or not the drawdown was associated with a recession. Looking at the largest 10 drawdowns in the S&P 500 Index since 1925, which we do in Figure 3, all saw gains over the ten years subsequent to the depth of the downturn. In fact, aside from two 10-year periods that were bookended by distinct macroeconomic and/or geopolitical crises—December 1968 through December 1978; and March 2000 through March 2010—markets were higher ten years later even from the mark peak just before the drawdown.

These views further support the belief that the wiser approach tends to have been to have avoided what might otherwise have felt like a sensible strategy when confronted with market tumult: to sell out of stocks in order to avoid a further decline. The thinking simply accepts the notions that 1) you’ve already incurred paper losses that 2) may prove permanent if you “lock them in” by selling downtrodden investments, and that 3) you’re well unlikely to be able to time a reentry into the market (since you likely did not time the exit prior to the drawdown) if you were to sell down your equity exposure and, finally, that 4) the fact of the drawdown may tilt the odds of potential future return a bit more in your favor.

Fortuneteller Folly

That’s not to suggest there isn’t the potential for markets to fall further if a recession appears or worsens. And we would not necessarily be surprised if further downside were to fruit. This period of distress after the superior market gains from the depths of the COVID-19 decline in early 2020 has seen successive versions of more conventional wisdom falling away as more optimistic tones are confronted with an incrementally more dire situation. The war in Ukraine has proved longer lasting and more brutal than many initially thought likely. And global inflation trends have proved far more persistent than consensus found probable.

The potential fly in the ointment of the present situation: seems stock analysts have yet to reel in their expectations for profits over the following quarters in moves that could be seen as acknowledging the potential oncoming slowdown in macroeconomic growth. As a result, the U.S. stock market has become less expensive relative to expectations for profits in the near future. Some may argue those perhaps too-rosy expectations are bound to see downward adjustments and that a decline in those forward expectations might result in a further drop in the market. Conversely, since this potential mismatch is already widely known, investors may well have already incorporated a potential decline in corporate profits into their analyses. That is, the current drawdown may already reflect a reduction in earnings growth, perhaps even an actual decline in earnings, that might come as a result of a potential recession.

Regardless, it’s hard to know in advance how quickly the global economy will decelerate, and how contributory the U.S. economy will be in that deceleration. So, patience once again is demanded by a market that, per the norm, offers little in the way of tea leaves useful in supporting a change in investment approach.

With investment markets likely to remain volatile as macroeconomic trends evolve, we want to ensure all readers that we welcome any discussions you may wish to have regarding your financial situation, your thoughts regarding market events and otherwise.

Meantime, SRCM wishes everyone a safe and celebratory July 4th weekend!

Important Information

Signature Resources Capital Management, LLC (SRCM) is a Registered Investment Advisor. Registration of an investment adviser does not imply any specific level of skill or training. The information contained herein has been prepared solely for informational purposes. It is not intended as and should not be used to provide investment advice and is not an offer to buy or sell any security or to participate in any trading strategy. Any decision to utilize the services described herein should be made after reviewing such definitive investment management agreement and SRCM’s Form ADV Part 2A and 2Bs and conducting such due diligence as the client deems necessary and consulting the client’s own legal, accounting and tax advisors in order to make an independent determination of the suitability and consequences of SRCM services. Any portfolio with SRCM involves significant risk, including a complete loss of capital. The applicable definitive investment management agreement and Form ADV Part 2 contains a more thorough discussion of risk and conflict, which should be carefully reviewed prior to making any investment decision. All data presented herein is unaudited, subject to revision by SRCM, and is provided solely as a guide to current expectations.

The opinions expressed herein are those of SRCM as of the date of writing and are subject to change. The material is based on SRCM proprietary research and analysis of global markets and investing. The information and/or analysis contained in this material have been compiled, or arrived at, from sources believed to be reliable; however, SRCM does not make any representation as to their accuracy or completeness and does not accept liability for any loss arising from the use hereof. Some internally generated information may be considered theoretical in nature and is subject to inherent limitations associated thereby. Any market exposures referenced may or may not be represented in portfolios of clients of SRCM or its affiliates, and do not represent all securities purchased, sold or recommended for client accounts. The reader should not assume that any investments in market exposures identified or described were or will be profitable. The information in this material may contain projections or other forward-looking statements regarding future events, targets or expectations, and are current as of the date indicated. There is no assurance that such events or targets will be achieved. Thus, potential outcomes may be significantly different. This material is not intended as and should not be used to provide investment advice and is not an offer to sell a security or a solicitation or an offer, or a recommendation, to buy a security. Investors should consult with an advisor to determine the appropriate investment vehicle.

The S&P 500 Index measures the performance of the large-cap segment of the U.S. equity market.

One cannot invest directly in an index. Index performance does not reflect the expenses associated with the management of an actual portfolio.

Investing in any investment vehicle carries risk, including the possible loss of principal, and there can be no assurance that any investment strategy will provide positive performance over a period of time. The asset classes and/or investment strategies described in this publication may not be suitable for all investors. Investment decisions should be made based on the investor's specific financial needs and objectives, goals, time horizon, tax liability and risk tolerance.